Every once in a while customers complain that they are seeing "unauthorized" credit card charge(s) on their bank account. Customers attempted to place an order online, and the credit card declined for some reason but the bank account of a buyer shows that the charge went through. We (the merchant) look up our payment gateway and see multiple "declined" transactions. Customers ask us to remove the charge(s) for those transactions that were never approved in the first place. So, what is going on here? Let's start out with the customer's question and the merchant's response.

Q. I (the buyer) have tried to purchase an item online, but my credit card was declined. However, when I call my bank they are telling me the charge went through. My credit card company tells me that your company double charged my credit card, and you (the merchant) are telling me the order didn't go through. I trust my bank, so please remove the charge(s) from my bank.

A. The merchant is telling you the transaction was declined, and your bank is telling you it has been approved. Yes, your bank approved the transaction but the merchant's payment gateway declined the transaction so the entire transaction was declined even though your bank approved it. Merchant's payment gateway may have security settings that may have triggered a decline such as address and zip code verification. It is the way how the banks operate, so it's not your fault nor the merchant's fault. The merchant cannot remove the charge since it was never approved, so please do NOT ask the merchant to remove this charge. The charge will be in a "pending" state, and the money will never be taken out of your credit card account but the reserve will be put aside so it will reduce your credit limit until the transaction clears on its own within 2-5 business days. The bank will say "Ask the merchant to call in to cancel this transaction", but a merchant CANNOT call in on your behalf as the credit card companies will not share account information with non-account holders such as a merchant.

To understand why this is happening, you'll have to understand how credit card transactions are processed. For a full explanation, please read the Credit Card Processing Diagram with the explanation below.

1. When a buyer commits an order, the credit card transaction goes to the payment gateway provider such as Authorize.Net and forwards the transaction to the Merchant Bank's Processor.

2. The information is then sent to your bank ("issuing bank"), and your bank will either approve or decline the transaction based on the customer's available funds. If the transaction is declined by your bank, the transaction stops and there is NO problem. The customer's bank account will show the transaction declined and so will the merchant's processor so there is no reason to argue with the merchant or bank.

3. If the transaction is approved by your bank, now the transaction is once again going through a security check by the payment gateway company with billing information sent by the issuing bank. If the customer's entered address, zip code, and card code do not match with the credit card billing information provided by the issuing bank, the payment gateway may decline the transaction based upon the merchant's fraud security settings. This is the reason why your bank says it's approved, and your merchant says declined -- and, they are both right!! Your bank approved the transaction, but the payment processor declined the transaction.

To conclude, the net result of the transaction status is a failure as the payment processor declined the transaction even though your bank approved it. This transaction will NOT show up on your credit card statement as it is declined by the payment processor. To your bank, they'll see this transaction as approved and will temporarily hold ("reserve") this money until the payment processor claims the money (which will never happen as it is a declined transaction), or a specific time elapses with no action from the payment processor which then releases the reserve. The time it will take to release the fund varies from bank to bank, and it could take anywhere from 2-7 business days.

The reason for multiple "approved" transactions on your bank account may be due to multiple attempts on your part to submit the order when the payment processor declined the previous transaction.

Why would a payment gateway company scan a security check and decline the transaction when the issuing bank already approved the transaction? Credit card fraud is one of the fastest-growing crimes as more and more people are buying products and services online. When fraud occurs, the banks get their money back from the merchant and the customers get their money back from the banks (with a bit of hassle). It is the merchant who will lose money on fraudulent transactions. To protect merchants and buyers, payment gateway providers implemented additional security checks to prevent "possible" fraud.

Note: You may reproduce and distribute the contents of this article provided that you give full credit to the author ("Scott Seong"), and provide a backlink to this page from your webpage. The content shown below is borrowed from Authorize.Net, and we do not have the authority to grant permission to redistribute its content.

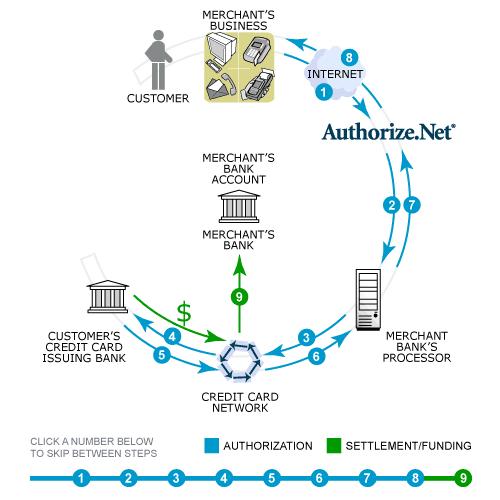

Credit Card Transaction Workflow Diagram Source: Authorize.Net

1. The merchant submits a credit card transaction to the Authorize.Net Payment Gateway on behalf of a customer via a secure Web site connection, retail store, MOTO center, or wireless device.

2. Authorize.Net receives the secure transaction information and passes it via a secure connection to the Merchant Bank's Processor.

3. The Merchant Bank's Processor submits the transaction to the Credit Card Network (a system of financial entities that communicate to manage the processing, clearing, and settlement of credit card transactions).

4. The Credit Card Network routes the transaction to the Customer's Credit Card Issuing Bank.

5. The Customer's Credit Card Issuing Bank approves or declines the transaction based on the customer's available funds and passes the transaction results back to the Credit Card Network.

6. The Credit Card Network relays the transaction results to the Merchant Bank's Processor.

7. The Merchant Bank's Processor relays the transaction results to Authorize.Net.

8. Authorize.Net stores the transaction results and sends them to the customer and/or the merchant. This step completes the authorization process – all in about three seconds or less!

9. The Customer's Credit Card Issuing Bank sends the appropriate funds for the transaction to the Credit Card Network, which passes the funds to the Merchant's Bank. The bank then deposits the funds into the merchant's bank account. This step is known as the settlement process and typically the transaction funds are deposited into your primary bank account within two to four business days.

Share this post

Leave a comment

All comments are moderated. Spammy and bot submitted comments are deleted. Please submit the comments that are helpful to others, and we'll approve your comments. A comment that includes outbound link will only be approved if the content is relevant to the topic, and has some value to our readers.

Comments (0)

No comment